Rent receivable is an asset account that represents rent that has been earned but not yet collected. When a tenant pays rent to a landlord, the landlord debits their Cash account and credits their Rent Receivable account. Accrued rent is a liability that represents the obligation incurred for the use of an asset owned by a third party. Typically accrued rent is recorded for the use of a building or property that has not yet been paid for.

Accruing Rental Income

We call the period of converting a Debtor balance to Cash as credit period allowed to the tenant. Tenant – The party who rents the property and pays rent to the landlord is called ‘tenant’. Welcome to AccountingFounder.com, your go-to source for accounting and financial tips. Our mission is to provide entrepreneurs and small business owners with the knowledge and resources they need. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Example: Straight-line rent expense calculation

Write-offs, on the other hand, are the final step when it becomes clear that a receivable is uncollectible. This might occur after exhaustive collection efforts have failed, or when a tenant declares bankruptcy. Writing off a receivable involves removing it from the balance sheet, which directly impacts the income statement by recognizing a loss. This step is crucial for maintaining the integrity of financial records and providing a realistic view of the company’s financial position.

Deferred Rent under ASC 842 Explained with Examples and Journal Entries

Income and expense a/c is debited to record the journal entry of rent paid. In this example, the tenant uses their January 2022 incremental borrowing rate of 7%, and payments are made at the beginning of the month. Using these facts and LeaseQuery’s free NPV calculator, the present value of the remaining lease payments is $11,254,351. Utilizing accounting software like QuickBooks or specialized property management tools such as Yardi or AppFolio can streamline this process. These platforms not only help in tracking due dates and amounts but also in generating reports that provide insights into the aging of receivables.

Rent Receivable in Lease Accounting

This assessment helps in setting up an allowance for doubtful accounts, which acts as a buffer against potential losses. Tools like Microsoft Excel, with its robust data analysis capabilities, can be instrumental in performing these evaluations. The difference between the two accounts is that rent receivable is a balance sheet account and is reported at the end of the accounting period.

Gross Method Accounting: Principles, Impact, and Comparisons

- The clarity and specificity of lease agreements are paramount, as they directly influence the accuracy of financial records.

- Under ASC 842 any differences between the expense recognized and the actual cash paid are recognized in the lease liability and ROU asset.

- Example – On 1st January ABC Co. paid office rent amounting to 10,000 (5,000 x 2) for the month of January & February.

- This income statement doesn’t change once the rent accrual occurs, irrespective of the fiscal year you actually receive the payment.

- Deferred rent is a liability created when the cash payments and straight-line rent expense for an operating lease under ASC 840 do not equal one another.

Proper accounting of rent receivable and rent revenue is essential for accurate financial reporting. Deferred rent is one of the most commonly discussed items regarding the differences between ASC 840 and ASC 842. This article discusses the lease accounting treatment for deferred rent and how the changes in the lease guidance impacted its treatment.

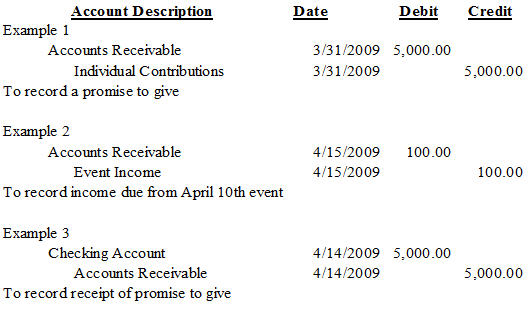

The income statement will reflect the total of all journal entries you make to the rental revenue account for accrued rent. This income statement doesn’t change once the rent accrual occurs, irrespective of the fiscal year you actually receive the payment. Moreover, the balance sheet will report the total balance of the outstanding rent receivables account as of the close of the fiscal year as a company asset. A debit to the rent receivable account and a credit to the rent revenue account may be recorded in the accounting system as part of a journal entry.

The journal entry is also used to record the exchange of goods or services for the rent payment. For example, if the customer is paying rent for the use of a space, the journal entry will record the rental payment and the space that the customer is using. This helps to ensure that the company is accurately tracking its income and expenses.

Future payments for rent-related to operating leases were previously off-balance sheet transactions. This was beneficial to lessees in that the obligation for those payments did not drive up the liability balance. However, ASC 842 aims to increase transparency for stakeholders rent receivable journal entry by including a lease liability and corresponding ROU asset on the balance sheet for operating leases. The management of rent receivables also plays a significant role in shaping various financial ratios, which are crucial indicators of a company’s financial health.

Leave A Comment